What to choose : NPS vs UPS

National Pension Scheme vs Unified Pension Shceme

4/20/20252 min read

When planning for retirement, choosing the right pension scheme can make a significant difference to your future financial stability. Two prominent schemes in India are the National Pension Scheme (NPS) and the Unified Pension Scheme (UPS). While both aim to provide long-term financial security, they differ in structure, tax treatment, and suitability based on individual goals.

What is NPS?

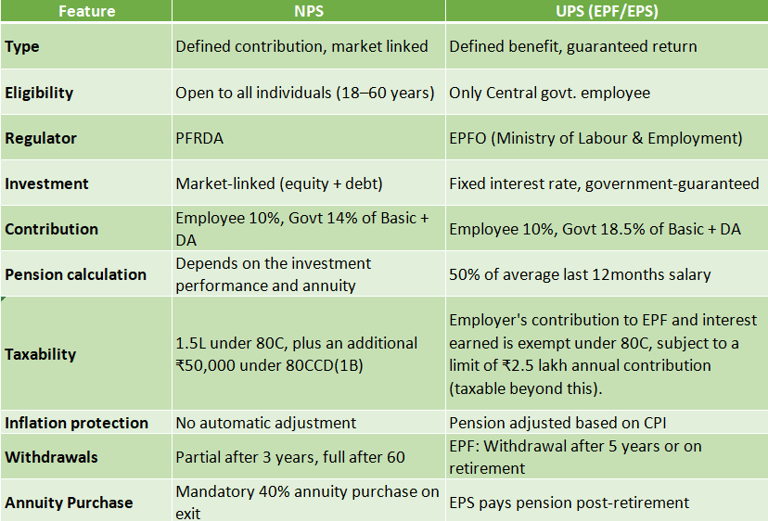

The National Pension Scheme (NPS) is a government-backed, voluntary retirement savings scheme regulated by the Pension Fund Regulatory and Development Authority (PFRDA). It is open to all Indian citizens aged between 18 to 60 years. Contributions made to NPS are invested in market-linked instruments like equities, government bonds, and corporate debt.

What is UPS?

The Unified Pension Scheme (UPS), introduced under the Employee’s Provident Fund Organisation (EPFO) umbrella, consolidates benefits of EPF, EPS (Employee Pension Scheme), and EDLI (Employee Deposit Linked Insurance). It is primarily available to salaried employees working in the organized sector and is managed by the Ministry of Labour and Employment.

To illustrate the difference, consider a hypothetical employee with a basic salary of ₹50,000 per month at retirement, with 30 years of service.

Under UPS:

Pension = 50% of basic pay= Rs.25,000 per month.

Gratuity = (Last Drawn Salary x 15/26) x Number of Years of Service = Rs.8,65,000/-

Total benefits include a guaranteed ₹25,000 monthly pension, inflation-adjusted (CPI), and the lump sum gratuity.

Under NPS:

Monthly contribution : Rs.12000/- (10% of basic and 14% employee contribution)

At 10% return: Future value = 2.71cr 60% lump sum (tax-free): 0.6 * 27100000 = Rs. 1.62 crore

Remaining 40% for annuity: Rs. 1.08 crore. Assuming a 6% annuity rate, annual pension = Rs. 7.97 Lakh, or Rs.66,400 monthly.

Both NPS and UPS cater to different needs: NPS offers potential for higher returns with market risks, ideal for younger, risk-tolerant employees, while UPS provides a guaranteed, inflation-adjusted pension, better for those nearing retirement employees. The decision hinges on age, risk appetite, and financial goals. Choosing between NPS and UPS depends on your employment type, investment risk appetite, and retirement goals. NPS suits those seeking flexibility and higher returns, while UPS offers stability and employer-driven benefits. Ideally, both can complement each other for holistic retirement planning.

For personalized retirement & pension planning, consult a SEBI-registered investment adviser to align your choice with your financial goals.

Registration Granted By SEBI (INA000020208), Membership Of BASL (BASL2266), And Certification From NISM In No Way Guarantee Performance Of The Intermediary Or Provide Any Assurance Of Returns To Investors. Investment In Securities Market Are Subject To Market Risks. Read All The Related Documents Carefully Before Investing. We are Fee Only Advisers. We prioritize customer over commission.

Copyright © 2025 Neha Sinha - All Rights Reserved.