Embarking your investment journey? Cut through the clutter with our expert advice.

Comparison of two products.

2/21/20252 min read

Are you new to the world of investing or feeling overwhelmed by the numerous options available? You're not alone. With so many choices, it can be daunting to decide where to start. This article breaks down the complexities of investing into a simple, easy-to-understand comparison of two popular investment options. Let's dive in and explore a straightforward approach to investing, perfect for beginners or those seeking clarity in a crowded market.

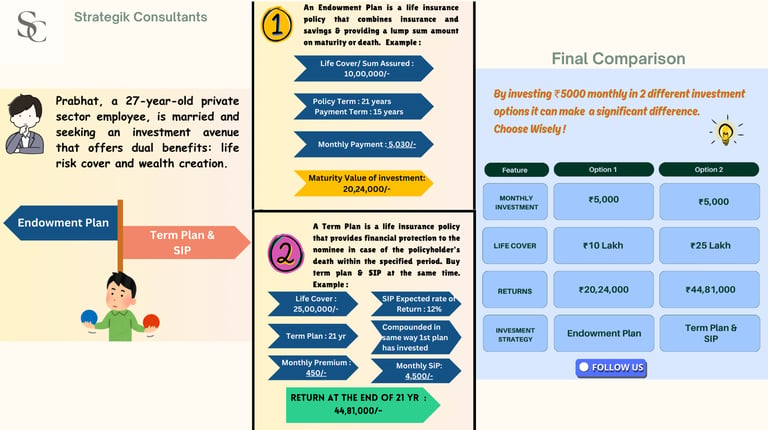

Prabhat, a 27-year-old private sector employee, is married and seeking an investment avenue that offers dual benefits: life risk cover and wealth creation. He googled, to find out the best option and landed himself into confusion. He had an investment budget of Rs.5000/- per month. To help resolve the dilemma of where to invest and maximize his benefits, let's take a closer look at the following illustration...

Option 1 – Buying an Endowment Plan.

An Endowment Plan is a life insurance policy that combines insurance coverage with a savings component. You pay a premium for a fixed term, and upon maturity, receive a lump sum payout. It provides financial security, disciplined savings, and tax benefits, making it a popular long-term investment option. While endowment plans offer the dual benefit of life cover and savings, the returns on these plans are typically modest. This is because a significant portion of your premium goes towards providing life insurance coverage, which reduces the potential for higher returns. If you are opting a traditional plan then the returns may range from 4% - 6%, unfortunately, the returns on endowment plans often struggle to match the rate of inflation. Suppose you bought a traditional endowment plan having:

Life cover = 10 Lakh

Term = 21 years

Premium/Monthly = 5030/-

Maturity Value = 20,24,000/-

Option 2- Buying a Term Plan and Investing in SIP.

A Term Plan provides life coverage for a fixed period, ensuring financial security for your loved ones. In case of your unfortunate death during the term, a death benefit is paid to your nominees. There's no maturity benefit if you survive the term. It's a budget-friendly way to safeguard your family's financial future. A term plan offers pure risk cover, making it a cost-effective option for those seeking hassle-free risk coverage. The premium will be 10% of what you pay to buy an endowment plan. The remaining fund can be used to invest through SIP in mutual fund i.e. 4,500/-, lets understand the figures.

Life Cover = 25 Lakh

Term = 21 years

Premium/Monthly = 450/-

SIP Investment = 4,500/- for 21 yr

Expected Rate of Return = 12%

Maturity value = 44,81,000/-

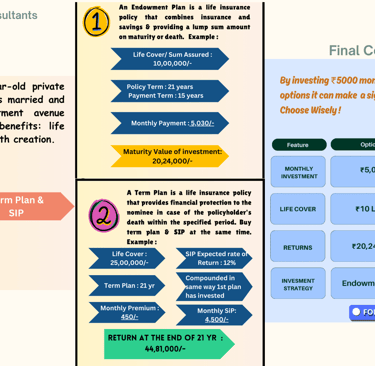

Conclusion: Before investing, it's crucial to grasp the nuances of each product and its potential returns. A thorough understanding can make all the difference. By investing 5000/- monthly, Option 1 offers a Risk cover of 10L and return of 20L whereas Option 2 offers a Risk cover of 25L and return of 44L.

Choose wisely. Take the time to evaluate your investment options carefully, and don't hesitate to seek guidance if needed. Your financial future depends on it.

Registration Granted By SEBI (INA000020208), Membership Of BASL (BASL2266), And Certification From NISM In No Way Guarantee Performance Of The Intermediary Or Provide Any Assurance Of Returns To Investors. Investment In Securities Market Are Subject To Market Risks. Read All The Related Documents Carefully Before Investing. We are Fee Only Advisers. We prioritize customer over commission.

Copyright © 2025 Neha Sinha - All Rights Reserved.